Once you have an understanding about how things work, the next step is to know what you need to do to make them work for you. I remember reading an idea by Zig Zigler that really stuck with me.

He said to imagine you were walking in a large field and above you was a large spaceship that was just hovering. Every few minutes it would smash down and decimate whatever it touched. That was the only information you had.

As you watch it, you begin to make connections about how often, how hard, and how much area it smashed. Hopefully you made the most important connection of where you need to stand not to get caught in it's path.

The main point being, you don't need to understand the machine, you just need to understand where to move to stay out of its path to survive. You don't need to always understand the inner workings of something, however you need to respect it and learn where to put your money so it stays safe and grows.

That is like the stock market and investing.

Luckily, there are so many free tools out there for you to learn, understand, and do your own research when it comes to the money and financial freedom!

He said to imagine you were walking in a large field and above you was a large spaceship that was just hovering. Every few minutes it would smash down and decimate whatever it touched. That was the only information you had.

As you watch it, you begin to make connections about how often, how hard, and how much area it smashed. Hopefully you made the most important connection of where you need to stand not to get caught in it's path.

The main point being, you don't need to understand the machine, you just need to understand where to move to stay out of its path to survive. You don't need to always understand the inner workings of something, however you need to respect it and learn where to put your money so it stays safe and grows.

That is like the stock market and investing.

Luckily, there are so many free tools out there for you to learn, understand, and do your own research when it comes to the money and financial freedom!

“The more that you read, the more things you will know. The more that you learn, the more places you'll go.”

― Dr. Seuss

Understanding it all

This class period is solely dedicated to helping you with the following three steps:

Financial Words 101Understanding finance, terms, and the inner-workings

|

Opening AccountsTeaching you what type of accounts to open

Savings/Investing/ Retirement |

Building Your AccountsShowing you how to build them and what you can put in them

|

Financial Words 101

Money can be confusing so this section is dedicated to helping you understand basic financial terminology. If you don't know the words, how can you understand financial freedom?

Save

Saving= Anything you have left over after you've paid your monthly expenses

(Checking/Banking Account)

Short Term Goals (Taxable Accounts)

Invest

Investing= Money you allocate towards building wealth and financial freedom

(Market/Investments)

Long Term Goals (Tax-Advantage Accounts)

Where you can keep your money

Your money basically can be placed into different vehicles to be saved or invested. Imagine you place a dollar bill inside of a vehicle and it travels somewhere where it can grow bigger. Some vehicles are slow and safer simply protect and shield it from harm and others are fast and involve risk as they attempt to grow it.

Get in George! Where shall we go today?

Checking Account

Your checking account is where you keep money (generally not making money) within a financial institution (bank) where you are able to deposit (put money in) and where you are able to withdraw (take money out).

Savings Account

Your savings account is where you earn interest (money on your money) when you keep money in the account. The bank does this so they can use your money to make more money.

The Markets

A place where stocks (equity ownership in a company), bonds (form of debt in which you are the bank being paid back), and commodities (bulk goods and raw materials that trade inside of the market). There are different vehicles (accounts you put your money into as they work inside the stock market). See below:

Tax-Advantage Accounts

The Government gives you a tax break/shelter if you save money in these accounts and agree not to use until you are the age 59 1/2 or older.

401 (k)

403 (b)- Mostly what educators have access to (Read this)

Traditional IRA

Roth IRA

Roth 401 (k)

Self-Directed IRA

Think of these accounts as ones where you put money in for the long haul of your life. You are paying your future self with now money.

Taxable Accounts

A taxable account is money you already saved, and already paid taxes on and that you would like to invest. Money can be taken out at any time, however all the profits and dividends are taxed.

Individual

Joint

Money Market Mutual Funds

Real Estate

Think of these accounts as ones where you put money in with the idea that you can have access to the money in the short term. You are using your now money to pay your near future self.

The Government gives you a tax break/shelter if you save money in these accounts and agree not to use until you are the age 59 1/2 or older.

401 (k)

403 (b)- Mostly what educators have access to (Read this)

Traditional IRA

Roth IRA

Roth 401 (k)

Self-Directed IRA

Think of these accounts as ones where you put money in for the long haul of your life. You are paying your future self with now money.

Taxable Accounts

A taxable account is money you already saved, and already paid taxes on and that you would like to invest. Money can be taken out at any time, however all the profits and dividends are taxed.

Individual

Joint

Money Market Mutual Funds

Real Estate

Think of these accounts as ones where you put money in with the idea that you can have access to the money in the short term. You are using your now money to pay your near future self.

Real Estate

Real estate is a tangible asset (you can own it) and a real property. This includes lands, buildings, and other real improvements.

Crowdfunding

Crowdfunding is basically putting in your money with other people to increase your purchasing power (buying more than you could alone).

Luxury Assets (Possessions)

Luxury assets are tangible asset (you can own it) and can be considered a collectible. This includes diamonds, fine art, cars, watches, and other jewels.

Cash in hand

This is basically just holding onto currency (cash money) and means you have liquid assets (spend at your leisure).

Key financial terms to know

Assets- everything that has economic value and can be sold/traded for money.

Liabilities- everything you owe/debt that you are financially and legally responsible for.

Personal Income- a person's total earnings from salary, wages, and bonuses during a specific time period of work.

Taxes- "a compulsory contribution to state revenue, levied by the government on workers' income and business profits, or added to the cost of some goods, services, and transactions."-Google

A Beginner's Guide To America's Tax System

A Beginner's Guide To America's Tax System

Budget- a plan for how you are going to use your money. How you are going to save, invest, and spend your money! Budgets are like diets and are hard to follow. Instead replace your budget mindset with a financial mindshift on money.

Credit Score-what the creditors (people lending you money) look at when determining your credit worthiness. It ranges from 300 – 900 points and also balances a variety of factors about your financial behavior through past, current, and future scenarios. It is basically reflects the likelihood that you will repay your debt and how much risk is involved.

Loan - a sum of money lent at a specified interest rate to make a purchase that requires more money than a person has.

Term -the time/number of months that the loan will take to be paid off.

Principal - the amount you’ve initially borrowed.

Interest - the money you are charged for borrowing a loan. The lower the better.

Insurance- a practice/arrangement by which a company or government agency provides guarantee of compensation for specific loss, damage, illness, or death in return for payment of a premium. Must have!

Interest Rate - the cost of borrowing money, expressed as a percentage, usually over a period of one year. The lower the better when paying.

Compound Interest - interest earned on previously accumulated interest as well as the principal.

Capital Gains- when you sell an investment that is worth more than when you purchased it for. Taxes could be owed on the profits.

Losses- when you sell an investment for less than you initially paid for it. Reduction in the taxes you might owe.

Losses- when you sell an investment for less than you initially paid for it. Reduction in the taxes you might owe.

Side Hustle-creating money from doing something other than your main source of income. Earning more money than your typical job/profession creates.

Pension-a regular payment/s made to a person retired from an investment fund (large pool of money) that a person or employer contributed into while that person was employed (working). Years of service and requirements apply.

Even more key financial terms to know!

Opening Accounts

Knowing your options is half the battle when it comes to building wealth. This section is dedicated to showing you what options you have when it comes to your money. Find the right place that best fits your life!

Account options

|

|

I would be willing to wager that the majority of you have checking and saving accounts, however it is a good idea to look at and compare new options. I am a huge fan of the information that nerdwallet provides and their online comparison tools is a solid way to determine what best fits your life and your financial needs. Start comparing now!

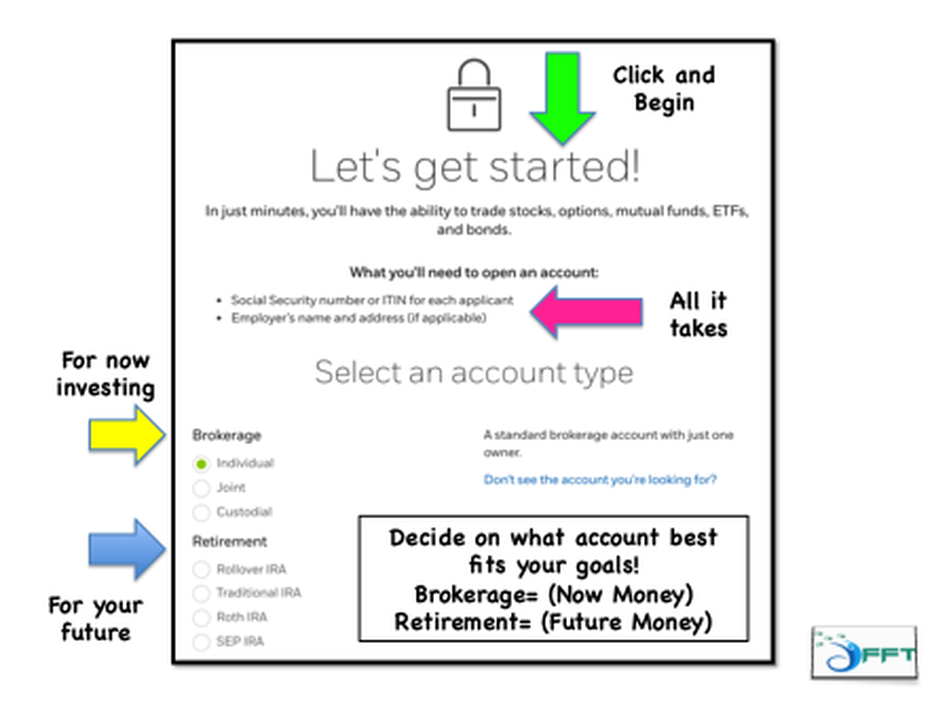

Investment/retirement accounts are going to get you into the financial freedom lane. These accounts are where you take your funds (money) to make investments into stocks, bonds, mutual funds (group of stocks/bonds), Etf's (group of stocks/bonds). Take a look at your options when it comes to amount needed, ratings, and what each brokerage (where you invest) offers and find the best fit for you. I included a link to E-Trade since that is what I personally for a few of my accounts.

Investment Accounts

Opening an Investing/Retirement Account

I am a huge fan of E-Trade for investing and retirement accounts. They have a user-friendly platform that is geared for the most novice investor, yet it offers resources, tools, and advancements that is waiting for you when you gain the confidence with your investing.

I am sure there are other brokerages out there so here is a solid resource to help you learn, compare, and discover which is the best fit for your needs.

I am sure there are other brokerages out there so here is a solid resource to help you learn, compare, and discover which is the best fit for your needs.

Building Accounts

You now understand the lingo, you have chosen what account(s) best fit your needs, and now you have to decide what to put in them to get your money to grow.

Food Shopping and Building a Portfolio

1. Imagine that your shopping cart is your investment vehicle (403b, IRA-Roth/Traditional, or Investment account)

2. Have a shopping list/plan (how I learn and research) before you even go. When you fail to plan, you are planning to fail. Once you know what you need in your cart (portfolio) based upon yourself, your financial goals, your investing timeframe then you can begin to feel confident about your purchases.

Determine the appropriate asset allocation (Conservative/Aggressive)

Building your portfolio (stocks, bonds, mutual funds, etf's)

Balancing percentages for your holdings (analyze and reflect on your purchases)

Rebalance (capital gains/losses and tax implications)

3.Realize that there are many stores (brokerages) you can make the purchases at so find a store you trust, you are comfortable with and that makes it easy to stay on track with your goals and strategies.

4. Look for the healthiest foods (stocks, bonds, etf's, mutual funds) that are going to be the best for your body and mind over the long haul (stable, growth/value, and minimal risk). The foods you put into your body decide how your body feels and acts and the same is true for your portfolio. The stocks, bonds, and funds that you have in your investment vehicles are going to determine how your money behaves and treats you.

5. Shop for the best deals (either low fees or at stocks/funds at good prices). Learn to look for deals, promo codes, and incentives when it comes to making purchases. Remember (PVC) price, cost, and value. Price is what you pay. Cost is the amount/inputs it took to produce/create or fundamentals/info about it . Value is the worth they provide you. So think about all 3 when you make an investment.

What is the price you pay for a stock/fund (Etf/mutual fund)?

What is cost you are incurring on your money for making the purchase?

Are you giving your money the best chance to grow?

What value are you getting from making the purchase?

Basically, are you getting the investment for a great price, value and does it align with your goals?

6. Understand that sometimes great purchases (a healthy apple- not the Apple stock) can sometimes still come with risk (bruised and mushy). Sometimes things you purchase while shopping might turn into huge hits when you bring them home. Sometimes you get lucky, however investing is very complex so make it as simple as possible by realizing the only things you really can control are:

Your emotions

Your risk

The cost

When you purchase/sell

The financials around it all (taxes, capital gains/losses)

7. You are human and sometimes you will see an impulse purchase (a candy bar at the checkout). If you must make some risky purchases (check out one of mine) than make sure you limit it to 10% of your portfolio. Example- if your total portfolio is $10,000 than $1,000 of it should be the maximum you spend on particular investments.

8. As you are finishing your shopping make sure you have a strong grasp on what you purchased, the prices you paid, and the total cost to your overall wealth. Have a system in place where you can easily view and track your food shopping (expenses) and your portfolios (what I use). Life is hard enough, why not make things easy when you can?

9. Remember that it takes time and energy to do both, however the goal is to make both as easy as possible. Learn to make your food shopping about making the healthiest food choices that are going to positively impact your life and health. Learn to build strong investing habits around building and growing your portfolios by staying calm, focused, and by looking at the big picture. Example- Focus on the fact your entire portfolio is up 2% instead of the fact that one fund maybe down 5% in a day.

10. Both are essential to survival (if you don't eat you die and if you don't invest you won't get financial freedom). Learn to embrace doing both (food shopping without kids is amazing) and realize that both have amazing potential to make your life healthier and wealthier now and later.

2. Have a shopping list/plan (how I learn and research) before you even go. When you fail to plan, you are planning to fail. Once you know what you need in your cart (portfolio) based upon yourself, your financial goals, your investing timeframe then you can begin to feel confident about your purchases.

Determine the appropriate asset allocation (Conservative/Aggressive)

Building your portfolio (stocks, bonds, mutual funds, etf's)

Balancing percentages for your holdings (analyze and reflect on your purchases)

Rebalance (capital gains/losses and tax implications)

3.Realize that there are many stores (brokerages) you can make the purchases at so find a store you trust, you are comfortable with and that makes it easy to stay on track with your goals and strategies.

4. Look for the healthiest foods (stocks, bonds, etf's, mutual funds) that are going to be the best for your body and mind over the long haul (stable, growth/value, and minimal risk). The foods you put into your body decide how your body feels and acts and the same is true for your portfolio. The stocks, bonds, and funds that you have in your investment vehicles are going to determine how your money behaves and treats you.

5. Shop for the best deals (either low fees or at stocks/funds at good prices). Learn to look for deals, promo codes, and incentives when it comes to making purchases. Remember (PVC) price, cost, and value. Price is what you pay. Cost is the amount/inputs it took to produce/create or fundamentals/info about it . Value is the worth they provide you. So think about all 3 when you make an investment.

What is the price you pay for a stock/fund (Etf/mutual fund)?

What is cost you are incurring on your money for making the purchase?

Are you giving your money the best chance to grow?

What value are you getting from making the purchase?

Basically, are you getting the investment for a great price, value and does it align with your goals?

6. Understand that sometimes great purchases (a healthy apple- not the Apple stock) can sometimes still come with risk (bruised and mushy). Sometimes things you purchase while shopping might turn into huge hits when you bring them home. Sometimes you get lucky, however investing is very complex so make it as simple as possible by realizing the only things you really can control are:

Your emotions

Your risk

The cost

When you purchase/sell

The financials around it all (taxes, capital gains/losses)

7. You are human and sometimes you will see an impulse purchase (a candy bar at the checkout). If you must make some risky purchases (check out one of mine) than make sure you limit it to 10% of your portfolio. Example- if your total portfolio is $10,000 than $1,000 of it should be the maximum you spend on particular investments.

8. As you are finishing your shopping make sure you have a strong grasp on what you purchased, the prices you paid, and the total cost to your overall wealth. Have a system in place where you can easily view and track your food shopping (expenses) and your portfolios (what I use). Life is hard enough, why not make things easy when you can?

9. Remember that it takes time and energy to do both, however the goal is to make both as easy as possible. Learn to make your food shopping about making the healthiest food choices that are going to positively impact your life and health. Learn to build strong investing habits around building and growing your portfolios by staying calm, focused, and by looking at the big picture. Example- Focus on the fact your entire portfolio is up 2% instead of the fact that one fund maybe down 5% in a day.

10. Both are essential to survival (if you don't eat you die and if you don't invest you won't get financial freedom). Learn to embrace doing both (food shopping without kids is amazing) and realize that both have amazing potential to make your life healthier and wealthier now and later.